Unfortunately, most of these will be graphs of supply and demand. I don't really like using supply and demand arguments, especially in graphical form, because I think that this form of argument is often used in place of actually understanding the situation. It is easy to fool yourself both of your understanding and of the certainty of a conclusion by drawing it up in a technical-looking graph. I suppose this is because graphs can convey the illusion of mathematical certainty and precision of thought, even when it isn't necessarily present. In the case I will be discussing -- the incidence of sales tax and the possibility of attainment of a monopoly price -- I think that there has been some confusion about what a graph actually shows, which I think has led a lot of people into a conceptual error.

I will begin with a basic layout of supply and demand schedules to show how subjective valuation information can be used to construct graphs of supply and demand. Then I will do something a bit unusual with them to make a point about what I think are errors of analysis applied to the types of graphs Rothbard uses in discussing monopoly and the incidence of taxation.

***

In the earlier chapters of Man, Economy and State, Rothbard describes how supply and demand schedules can be used to create graphs of supply and demand and determine market pricing behavior, which, for my purposes, can be condensed into something like this--

Suppose that 7 buyers and 7 sellers of a certain good meet at a marketplace, and their individual subjective valuations for the item are as follows --

Each seller has one item for sale, and each buyer is interested in purchasing one item.

From this information, it is easy to arrive at the available supply and demand of the item. Supply can be determined by counting how many sellers would be willing to sell their item at a given price or below. Demand can be determined by counting how many buyers would be willing to purchase the item at a given price or above. This gives the following supply and demand schedules --

Here one can see that under these conditions, 4 items will be sold -- at the price-point where quantity supplied and demanded are equal -- and the market price will be $3. Sellers 4,5,6 and 7 will sell to buyers 1,2,3 and 4. Graphing the two curves gives the following supply and demand graph --

This is, of course, rather crude. For most markets, there will be many more than 7 buyers and sellers, and multiple items will be bought and sold, etc. I will also neglect Rothbard's discussion about the discontinuity of the graphs (basically, supply and demand cannot be continuous mathematical functions because each valuation is discrete and corresponds to an individual) because it isn't really relevant here. This is just an illustration.

There are two far more important reasons why this analysis does not directly apply to normal markets. The first is that in this case, many of the sellers have some considerable valuation of the item in question. Such a situation might apply at a flea-market or garage sale, but most of the time, sellers simply want to sell whatever they have produced because they have no use for their inventory themselves and usually do not wish to store it. At any given time, the supply curve will tend to be vertical or near vertical at whatever quantity is presently being held, and the seller will simply take what money he can get on the market for it. If he has made a mistake and oversupplied his market, he will cut back production going forward, but he can hardly withold existing product for long because he has bills to pay and must put his capital back to work.

The second big reason is that this analysis is kind of like playing poker with the cards up. The whole game of poker consists in not knowing what cards the other players have. Likewise, in a market, nobody is going to reveal his own subjective valuation for others to see, so buyers and sellers are operating in the dark. Each one is really operating on only two data points -- his own valuation, and the price the item has exchanged for in the past. Everyone knows the 'going price' for the item in question, and what he himself is willing to pay (or be paid) for it. Once the 'going price' on the market is established, buyers are not going to offer much more, and sellers are not going to accept much less, until such time as it is clear that conditions have changed.

In the extreme, a market as experienced by its participants might really 'look like' the following --

The market price is X, there is Y quantity available at this price, and that's that.

So, in practice, supply and demand curves will be 'experienced' by buyers and sellers in a very different fashion than he first graph would suggest. This is important to understanding Rothbard's arguments. All the graphs he uses to argue about monopoly and the effects of taxation come with the important modifier of expressing the demand curve 'as it is experienced by an individual producer.' In other words, he is not drawing graphs of subjective valuation schedules, he is drawing graphs of demand as experienced by firms competing for consumer spending.

Drawing a horizontal line through the market price of the first graph reveals an important concept that this way of viewing things will tend to overlook --

The effect of markets is to cause transactions to occur at a uniform price regardless of the valuations of the individuals making the transaction. All one can know is that the exchange took place because the two parties valued the object differently, and therefore, the uniform rate of exchange established by the market will in large part not reflect the valuations of most of the buyers and sellers who engage in trading. Only for marginal participants -- those with valuations very close to the market price -- will the price reflect their actual valuations.

For the others, there is a substantial 'consumer surplus' of value which the trader enjoys because he has not had to pay anything close to his own valuation of the good in order to acquire it. If the reader has ever thought to himself, 'Wow! What a great deal!' he is giving expression to this phenomenon. In fact, if one thinks about it, most purchases really are of this type. It is what free-exchange is all about, mutually beneficial transactions, and is one of the very great things about markets. But as far as this discussion is concerned, the existence -- indeed, the ubiquity -- of consumer surplus means that for the vast majority of buyers, a higher price of the good would not have dissuaded the buyer from making the purchase in and of itself.

What keeps prices down -- and up, for that matter -- is the existence of choice. It is because there were multiple sellers that the high-valuation buyers did not have to pay their full subjective valuations to receive the good. Likewise, it is because there were multiple buyers that the sellers did not have to settle for a price exactly equal to their own valuations. If there had been no choices of whom to do business with, buyers and sellers would have been forced to deal with only one other party, who could have named his price right up to the highest or lowest valuation as it served his interests.

In terms of demand curves, the existence of choice -- which is to say, competition -- tends to flatten the curve as it moves beyond the market price. Other sellers will accept the market price, so why should the buyer offer more? Thus, the demand curve as experienced by an individual producer will not reflect the actual valuations by consumers. Each individual producer will experience a high elasticity of demand above the market price. A higher price will meet with a drastic reduction in quantity demanded, such that total revenue falls if there is any attempt to raise prices. Each producer will also likely experience a high elasticity of demand below the market price as well, as buyers of his competitors goods switch to his good, though for the purposes of this discussion this is mostly irrelevant since it will not profit the producer to do so.

What will the demand curve look like under these circumstances, and from this point of view? It will probably be a little different for each product, but in general, I should think there would be some sort of 'bend' near the equilibrium price point. Above this point, buyers of the good will change their preference to another competing good, and below this price buyers of competing goods will migrate to this product. I would think that these two processes would occur at different rates, since there will generally exist at least some 'product loyalty' which will probably differ in some degree from one product to the next. So, it is impossible to say just exactly what the 'bend' will look like, and it may not be noticeable at all in extreme cases of practically no loyalty or an indistinguishable difference of loyalty. But in any event, in a competitive market the curve will be relatively flat above the market price, and at some quantity the market will reach 'saturation' -- i.e. it won't go to infinite demand at zero price, simply because some price exists for storage, transport, etc.

The point of all of this, though, is that the upper end of the curve is flat not because of demand schedules, but because of competition. The market price is determined by the marginal buyers, and in a sufficiently competitive market, almost all buyers become marginal from the point of view of individual producers.

Rothbard's arguments about monopoly and the incidence of taxation turn on elasticity of demand. He claims that prices cannot be raised so long as the demand curve is inelastic above the market price, which is why 1) a sales tax can never be 'passed forward' on to consumers, but only backwards to the factors of production, and 2) a monopoly can never succeed in raising prices without state intervention. The argument that is often made is that if prices could be raised, the sellers would have already raised them. Prices are already as high as they can possibly be, so that a tax or a monopoly premium cannot be profitably added on. Demand would fall too dramatically to make this strategy profitable. He makes this argument in several other creative forms, but they amount to the same thing.

Hopefully, it is immediately clear from my discussion why these arguments do not hold, but just in case it isn't, I will walk through some different scenarios for the resolution of a new sales tax imposed on a product. Rothbard is correct that if the demand curve is inelastic above the market price, then prices cannot be raised. Where he is wrong is in assuming that the shape of the demand curve will not change in response to the change of situation. By making the arguments that he does, he assumes that the demand curve takes the shape that it does purely as a result of demand schedules, and ignores the effect of choice and competition -- which is to say, the actions of producers -- in producing its 'apparent' shape. The concept of consumer surplus is ignored.

Or maybe he just forgot about it since he had discussed it about a thousand pages earlier.

***

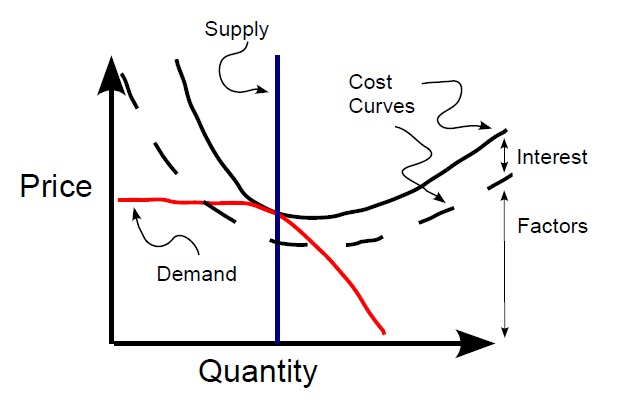

First, I'll look at a free-market example of the market 'as experienced by an individual producer.' I've drawn in a demand curve, the market price, and cost curves. Rothbard uses a number of these graphs in his discussion, however, I think they were a bit unrealistic. I made a curved, highly elastic demand curve -- implying a highly competitive market, being as generous to Rothbard as possible -- but a very different set of cost curves. Rothbard's curves look like the nose of a torpedo, which is silly.

There is a second, dashed cost curve which represents the 'cost' due to interest. This is important for understanding how the market will 'digest' the imposition of a new tax. Capitalists expect a return on their capital. In a competitive market at equilibrium, this will be the natural rate of interest, and will be the same for all forms of capital. Any change in the rate of return -- for example, the emergence of an enrepreneur's profit above the natural rate of interest, or a market change which makes collecting even the natural rate impossible -- will cause behaviors to change such that this disparity is eliminated. At equilibrium, there is no entrpreneurial profit, and every factor and all capital receive the same rate of return (I am ignoring differences in wages since human beings have no capitalization value and are not 'for sale').

The cost curve therefore incorporates the interest due to capital, plus factor costs, and no entrepreneurial profit. In this example, I will assume an interest rate of 5% and a newly imposed tax of 7%, which I have added to the cost curve such that it absorbs all of the interest due to capital and imposes a 2% loss on top of the loss of interest --

This assumes that factors have already been paid, and the capitalists are stuck selling a perishable good at a loss due to the imposition of the tax. Rothbard would argue that this is the case because, once the product had been produced, the costs are out of the picture in the past and the product must simply be sold for whatever it can fetch on the market. Supply is what it is, demand is what it is, and the price will therefore be what it will be under these circumstances and the capitalists just have to live with it.

This assumes that there is no possibility for the capitalists to 'hold out' for a higher price, which may or may not be a valid assumption. As far as this essay is concerned, it depends on how the rest of the argument turns out. Since I have not finished the argument, I will pass over the point for now, but only use it to set up the situation and examine the elements which must be resolved.

In order to come back to equilibrium, the natural rate of interest must either be restored or this particular market niche must go into obsolescence. Supposing that the market does not shut down, there are two possibilities -- either factor prices must fall, or consumer prices must rise. These two possibilities are pictured below --

The capitalists may be forced to accept the loss upon the initial imposition of the tax, but they absolutely will not bear it going forward, at least not insofar as they are not owners of the factors and are operating purely as capitalists. In practice, this is almost never the case, as business owners usually do have a stake in the factors they are using. This may take the form of extensive land holdings and the like, or limited to nothing more than in managing the operation, which is a form of labor.

But in general, in a free market businesses purely as such do not bear the burden of such a tax over the long run because they do not have to. If nothing else, they can always redeploy their capital into another line of production.

So, in which direction will the market resolve itself? According to Rothbard, it is exclusively in such a direction that factors absorb the tax. I think he is wrong, that the burden may be passed in either direction depending on circumstances but is usually shared. I'll analyze four scenarios to see how it plays out, which shall hopefully make my point for me. In each case, I will broaden the base of the tax, and the question that will have to be answered is 'can the price be raised?' How this question is answered will determine who pays the tax. I will use a very mundane good for my example -- dishsoap.

***

The first scenario is easy. In this case, consider four or five major producers of dishsoap, making practically indistinguishable products. The tax is imposed on only one of the companies, say Company A. What will happen?

Will Company A be able to raise its price to cover the tax? That depends on whether or not consumers will switch to an alternative producer. Rothbard asserts that only a consumer can serve as judge to determine whether or not two products are 'different.' To be sure, this is correct, and is one of the points of this exercise. If there 'is' a difference, and consumers are 'willing' to pay for it, such that the demand curve is inelastic, then the producer may safely raise the price and the consumer will pay the tax.

But by Rothbard's own argument (again, correct in this case), if this had been the case, the producer would already have raised the price to collect an above-market profit. But an above-market profit is excluded by this scenario in that the market is at equilibrium and competitive (do you see where I'm going with this?)! Thus, the argument cannot apply. The price is what it is precisely because of competition, and if other producers do not have to pay the tax and are willing to accept the natural rate of interest, which is the definition of equilibrium, then the taxed firm cannot pass the tax on to the consumer.

From the other side, however, the firm cannot pass the tax on to factors of production, either. Total demand for dishsoap has not fallen (because the price has not been raised) so demand for factors of production for this good will not fall and the going rate for these factors will remain the same. If Company A cannot afford to pay the going rate for factors and still make a profit, other producers will simply bid away these factors and increase their own production to collect the natural rate of interest.

So, in this scenario, the taxed firm cannot make a profit and is destroyed. Perhaps that is what is meant by 'the power to tax is the power to destroy.' In any event, it illustrates why a tax must of necessity be fairly broadly based, and why it is impossible to single out and force 'corporations' to pay for things. Either the corporations will pass the burden on to someone else as the natural rate of interest reasserts itself, or they will cease to exist altogether.

***

Now consider the case that the tax is imposed on all of the dishsoap companies. Now, none of them can make a profit at current prices and still pay the going rate for factors. Where will the burden fall?

Will the consumer pay a higher price if it is raised? The consumer is no longer protected by the fact that there are other firms willing to produce 'the same' good at existing prices. But there are 'substitute' goods -- barsoap, handsoap, etc. Again, one is confronted with the issue of whether or not the consumer considers these goods to be 'different.'

The argument that the market is 'still competitive' begins to look squishy -- which is the point I'm trying to illustrate by broadening the application of the tax. Rothbard chooses to take this very philosophical, detached point of view that asks the reader to check his common sense at the door. Bar soap and dishsoap are different. They may substitute for one another, or they may not from any individual's point of view, but it is hard to argue that there will continue to be the same competitive dynamic no matter what is happening. What I am describing here is considered a different form of competition by most people -- a substitute good vs. an identical good -- but Rothbard wants to continue on as if there is no difference. To his mind, there is always competition. He has a point, as I'll show later, but I don't think it is the point he thinks it is. The consequence is different from what he predicts.

These kinds of taxes interfere with competition. Rothbard cannot continue to argue that competition will continue to keep the demand curve inelastic as competition is being whittled away. Since it is competition which shaped the upper end of the demand curve, he cannot continue to assert that inelasticity prevents price increases as the demand curve itself changes.

But back to the concrete example. To the degree that consumers prefer using dishsoap to making do with other goods, the demand curve may shift upwards. Since there can be no other firms producing dishsoap who can make the natural rate of interest at existing prices, there is nothing to prevent the firms from raising the price to some new equilibrium point, at which a non-marginal number of consumers switch to using a non-taxed good. This will of course depend on the degree to which consumers consider other goods interchangeable with dishsoap.

In addition, factor prices may fall this time. There are no untaxed dishsoap producers who can bid factors away. There are, however, barsoap and other such manufacturers who might do so, depending on whether or not these materials were nonspecific to dishsoap and might be used for barsoap. To the degree that consumers accept such products as substitutes, the dishsoap manufacturers may be totally wiped out as in the last example.

But to the degree that consumers do not accept substitute goods, and to the degree that factors are specific to dishsoap, factor prices can be pushed down. I think this is most likely in such a case. It is probable that the tax will be borne by a combination of lower factor prices and higher consumer prices, depending on just how everything falls. But obviously, if this proves correct, it will not fall completely on either, for the reasons I have given. The demand schedule is not the same thing as the demand curve that individual businesses experience, so it cannot be argued that the demand curve is fixed.

Hopefully, Rothbard's case is looking weak at this point, but I'll keep going just to see how things play out. There are still good arguments in his favor which will need better examples to come out.

***

In this example, I want to consider a tax that falls on all soaps and detergents. Now, are there any substitute goods?

Rothbard would argue that there still are -- and to a degree, he is right! But I'll save that for later. However, it should be clear that these 'substitutes' are going to be considerably less 'substitutey' and more like completely different goods. Maybe one could get a dog to lick off the dishes before rinsing. I don't want to think about washing...other things...that way, but the message is clear -- it is very hard to argue that in this circumstance the market is still so 'competitive' that the demand curve doesn't change.

It is hard for me to imagine that factor prices would absorb the entirety of the loss, either. There is no longer any reasonable producer of 'soapy stuff' who does not pay the tax and may still make the natural rate of interest at present prices. The consumer surplus may take a beating, but I'm willing to bet that most people would fork over 7% more for soap rather than live without soap. They might cut back and conserve, but only 'marginal' buyers would balk altogether. And who 'wastes' much soap, anyway?

Finally, consider a tax on all goods, period. Now obviously, assuming the tax is effective and avoidance is impossible, this precludes any sort of goods substitution to avoid the tax. I'm not interested in that anymore; I want to look a this case to discuss something for which I do not know the name, but which I might call 'orthogonal competition.' Basically, all goods are in competition for the consumer's dollar all of the time, regardless of their function. Even if they're not in competition in the sense most people think of, nevertheless, they do compete in the broadest sense of bringing satisfaction to the consumer. Everything the consumer buys is an attempt to acquire utility, so to the degree that all goods are capable of supplying utility, they compete for the consumer's dollar.

This brings out the last good defense of Rothbard, and is one of the key insights, I think, of the Austrian school. I have used a form of this argument before myself in wage markets. It does not make sense to me that wages should show the large spread that they do if labor markets are truly competitive. It doesn't matter that there are so many positions for firemen and so many for teachers and so many for CEO's, etc., and only so many people qualified for such positions. Nevertheless, almost all people are either qualified or qualifiable for at least a few different positions, such that every position has multiple possible takers and every person has multiple possible opportunities. Further, every large wage differential presents an opportunity for entrepreneurs to devise a system of training and application of capital to qualify a lower wage person to perform the higher wage task. The labor market does not have to be perfectly competitive to be effectively competitive.

This is exactly the sort of argument Rothbard is using to defend the effective elasticity of demand, basically no matter what. And to be sure, his argument is partially correct, as I have shown. There is always a degree of substitutability, and so there is always a degree of elasticity above and beyond that provided by raw demand schedules. The question is what does it get him in the real world, which is how I've been arguing these examples.

I'm willing to accept that there will always only be effective competition rather than perfect competition in labor markets, so that a certain spread of wages on a free market will always exist, but should probably not be enormous -- say, within an order of magnitude, or two, or so. That just makes sense to me.

So, to return to the tax example. Suppose the tax is imposed across the board. What happens to the price of dishsoap and, say gold, at least according to me? Yes, I did choose these two deliberately.

To understand this, one must look at the whole picture. Each good will have an associated demand and cost curve. Again, the return to all capital must come to the natural rate, so factor costs must either fall, or prices rise, or a combination of the two, in each and every case. What one must do is determine the changes in patterns of demand to determine which way the axe will fall.

Clearly, the gloves of competition are off, as there are no producers at all who may make a profit at the natural rate and current prices, so demand curves are free to change. Factor owners are going to resist falling prices wherever they can, it is simply a question of where they may resist. Unfortunately, the problem is complicated by the fact that the factor owners are also consumers. So the changes in consumption will cause changes in factor income...which will cause changes in consumption, which will cause...

To a degree, this is a problem of all economics, and all sorts of sciences -- fleas on fleas on fleas. But if I may be allowed an approximation for the purposes of illustration, I think the general idea will shake out.

Suppose that, whether because of lower income, or higher prices, or merely because government is now claiming a portion of the economic product, that every consumer must give up a portion of consumption. What will happen?

Consider the following list of consumers, and assume that they are representative of the population --

The list of goods represents each person's ordinal preferences, from highest to lowest priority. If every consumer gives up one good, which goods will be given up, and what effect will this have? Yes, I chose a skewed example; in the real world there would likely be a great deal more variety and broader representations. But the point is to illustrate that it is possible for exceptions to Rothbard's rules to occur. Further, I doubt that many people would argue that basic necessities like food are not going to systematically get higher priority on most lists, and relatively non-essential items are likely to systematically appear lower.

Obviously, every consumer will give up consumption of his least preferred goods. In order for 'orthogonal competition' to force the tax onto the factors of production to the complete exclusion of consumer prices, it is necessary that all goods experience a roughly similar drop in demand -- that all varieties of goods be represented roughly proportionately at the bottom of lists. If there are any goods which are roughly so represented or overrepresented in the lower portion of these lists, then clearly prices cannot be raised much on these goods and factor prices will be forced downwards. But if there are goods which are generally high-priority goods, so that proportionally fewer consumers will give these up, then prices may rise on these goods, and factor prices will be relatively more firm. The forces of production will shift resources away from the marginal goods and towards the non-marginal goods.

To be more concrete, in these lists, dishsoap is lowest priority on only one list. So, total demand for dishsoap -- at whatever the fianl price -- will only fall about 20%. To the extent that the factors of production used for making dishsoap are non-specific, the fall in total demand for these factors will be somewhat less than this -- perhaps a great deal less, depending on their use in other markets. So, the fall in demand for these factors will be marginal, and therefore the change in price negligible. Therefore, the price of dishsoap must go up to restore the natural rate of interest for dishsoap production, and it can thanks to consumer surplus.

As for gold, it appears at the bottom of several lists. Demand for gold will be hit very hard. Prices cannot possibly rise in this market, and the factors of production can expect to bear the brunt of the loss.

***

In general, even though one can't predict exactly how things will fall out, there will be some marginal goods for which factor prices will be forced down, and others for which consumers will pay the tax. For most, it will likely be a combination of the two.

So, dishsoap really did compete with gold -- the problem for Rothbard is that dishsoap won too handily! Its demand curve shifted upwards in response to the imposed tax, while the curve for gold fell. Factors of production will tend to move from mining into soap production going forward. Rothbard's argument did work, partially, but it turned out that orthogonal competition was not enough to ensure sufficient elasicity in all cases. Rothbard's error was to assume that all goods were equally marginal -- that their prices 'couldn't' be raised. Elasticity can only be ensured when a large enough fraction of buyers are effectively marginal, and this is only the case when markets are sufficiently competitive. It is not a property intrinsic to demand schedules, and such a claim flies in the face of the ubiquity of consumer surplus.

Thank goodness it is wrong. I would hate to think about life in a world where such an argument was correct, and the benefit of every transaction hung on a knife's edge.

It doesn't take a lot to see how this argument about taxation applies to monopoly as well. The argument that a monopoly 'can't' raise prices because they are already as high as they can be does not hold water. This ignores the effects of competition in markets in shaping demand curves and denies the existence of consumer surplus. Rothbard's arguments about the difficulty of establishing and enforcing a monopoly are still valid, though difficult is not the same as impossible.

But when specifically asked about a lack of competition, 'elasticity of demand' is the one answer he can't use. And I, for one, do not find it persuasive in the slightest that since his oponents cannot sufficiently define 'monopoly' to his satisfaction that monopolies can therefore not be said to exist in a 'free market.'

I think they can, and do.

No comments:

Post a Comment