Yes, that's right, I said it -- deflation. The charts don't lie.

But note that this is a deliberate policy of the FED, not some spontaneous, out-of-control money-destroying spiral envisioned by the deflationists. It is also a small event, and might easily be reversed in coming weeks.

Note also that this does not negate the inflationist hypothesis. It is entirely consistent. The inflationary process inevitably creates inconvenient price distortions that must periodically be squelched by monetary tightening. I do not know what particular effect disturbs the FED at this time, but it appears to be taking action. If the trend continues, expect a major recessionary event, followed by a reinvigorated policy of monetary inflation.

But in the short run, bulls -- beware the matador's cape! Pay no attention to the FedFunds rate, for it only serves to conceal and distract attention from the deadly prick. It is meaningless. Bernanke is playing the same game he played in 2007. He claims to keep the rate "low" while refusing to add to the money supply. But the astute will know what this means -- Bernanke does not drive the rate lower. The market itself does. The FED is deflating, but Bernanke claims to keep the rate low and gets to play innocent bystander while the market crashes.

Or rather, to be somewhat more precise, the market distortions which have already occurred are finally revealed upon stabilization of the money supply.

The whole ruse works, of course, because the public believes in the interest rate narrative and the legitimacy of fiat currency regimes. I think even the FED believes it. It doesn't seem to occur to them that fraudulent accounting is just that -- fraudulent. It doesn't reflect reality. "Low" and "high" are relative terms. Relative to what? The Austrian school knows -- market rates!

It doesn't matter all that much whether interest rates are low or high, or rising or falling. What matters is whether money is being created or destroyed to influence the interest rate away from its market value. Right now, this very instant, the FED is destroying money while pretending to be "accomodating." Bernanke is behaving perfectly in character in doing this, as it is exactly what he has done in the past. He is being as tight as he can be, attempting to extricate himself from the FED's bloated balance sheet without visibly impacting markets. He won't be able to. The assets he bought cannot be sold in any meaningful volume without triggering a financial backlash and recession.

The money supply is falling very slightly, and the rate is what it is. The FED is not supporting financial markets. If it keeps to its present course, expect them to fall. When the free market assigns an interest rate of near zero, things are really, really bad.

So long as the public believes in this illegitimate system, it will never grasp the fact that virtually all financial calculations made under the monetary pretenses of a central bank are incorrect. Just a little bit of common sense should reveal this to even a mediocre intellect. Yet the delusion persists. Why does the public believe this charade? A few days ago, I would have called it a conspiracy. But it seems that is not the proper term.

Maybe I'll address the issue, at least to the best of my abilities, some other time.

Yes, that's right, I said it -- deflation. The charts don't lie.

But note that this is a deliberate policy of the FED, not some spontaneous, out-of-control money-destroying spiral envisioned by the deflationists. It is also a small event, and might easily be reversed in coming weeks.

Note also that this does not negate the inflationist hypothesis. It is entirely consistent. The inflationary process inevitably creates inconvenient price distortions that must periodically be squelched by monetary tightening. I do not know what particular effect disturbs the FED at this time, but it appears to be taking action. If the trend continues, expect a major recessionary event, followed by a reinvigorated policy of monetary inflation.

But in the short run, bulls -- beware the matador's cape! Pay no attention to the FedFunds rate, for it only serves to conceal and distract attention from the deadly prick. It is meaningless. Bernanke is playing the same game he played in 2007. He claims to keep the rate "low" while refusing to add to the money supply. But the astute will know what this means -- Bernanke does not drive the rate lower. The market itself does. The FED is deflating, but Bernanke claims to keep the rate low and gets to play innocent bystander while the market crashes.

Or rather, to be somewhat more precise, the market distortions which have already occurred are finally revealed upon stabilization of the money supply.

The whole ruse works, of course, because the public believes in the interest rate narrative and the legitimacy of fiat currency regimes. I think even the FED believes it. It doesn't seem to occur to them that fraudulent accounting is just that -- fraudulent. It doesn't reflect reality. "Low" and "high" are relative terms. Relative to what? The Austrian school knows -- market rates!

It doesn't matter all that much whether interest rates are low or high, or rising or falling. What matters is whether money is being created or destroyed to influence the interest rate away from its market value. Right now, this very instant, the FED is destroying money while pretending to be "accomodating." Bernanke is behaving perfectly in character in doing this, as it is exactly what he has done in the past. He is being as tight as he can be, attempting to extricate himself from the FED's bloated balance sheet without visibly impacting markets. He won't be able to. The assets he bought cannot be sold in any meaningful volume without triggering a financial backlash and recession.

The money supply is falling very slightly, and the rate is what it is. The FED is not supporting financial markets. If it keeps to its present course, expect them to fall. When the free market assigns an interest rate of near zero, things are really, really bad.

So long as the public believes in this illegitimate system, it will never grasp the fact that virtually all financial calculations made under the monetary pretenses of a central bank are incorrect. Just a little bit of common sense should reveal this to even a mediocre intellect. Yet the delusion persists. Why does the public believe this charade? A few days ago, I would have called it a conspiracy. But it seems that is not the proper term.

Maybe I'll address the issue, at least to the best of my abilities, some other time.

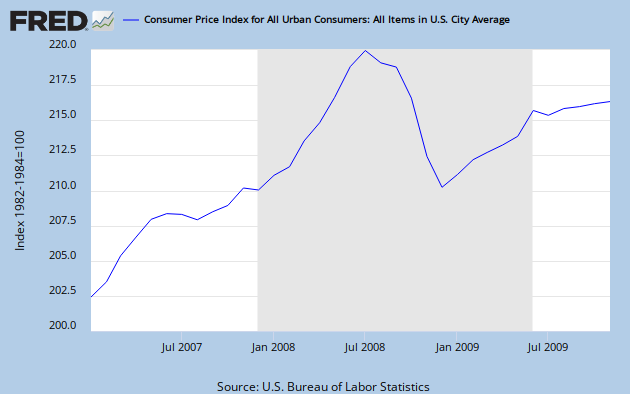

Friday, January 29, 2010

A Wee Little Bit of Deflation

M1 has ticked downwards in recent weeks. In addition, the Adjusted Monetary Base (AMB) has also turned down, indicating that the monetary contraction is being engineered by the FED:

Yes, that's right, I said it -- deflation. The charts don't lie.

But note that this is a deliberate policy of the FED, not some spontaneous, out-of-control money-destroying spiral envisioned by the deflationists. It is also a small event, and might easily be reversed in coming weeks.

Note also that this does not negate the inflationist hypothesis. It is entirely consistent. The inflationary process inevitably creates inconvenient price distortions that must periodically be squelched by monetary tightening. I do not know what particular effect disturbs the FED at this time, but it appears to be taking action. If the trend continues, expect a major recessionary event, followed by a reinvigorated policy of monetary inflation.

But in the short run, bulls -- beware the matador's cape! Pay no attention to the FedFunds rate, for it only serves to conceal and distract attention from the deadly prick. It is meaningless. Bernanke is playing the same game he played in 2007. He claims to keep the rate "low" while refusing to add to the money supply. But the astute will know what this means -- Bernanke does not drive the rate lower. The market itself does. The FED is deflating, but Bernanke claims to keep the rate low and gets to play innocent bystander while the market crashes.

Or rather, to be somewhat more precise, the market distortions which have already occurred are finally revealed upon stabilization of the money supply.

The whole ruse works, of course, because the public believes in the interest rate narrative and the legitimacy of fiat currency regimes. I think even the FED believes it. It doesn't seem to occur to them that fraudulent accounting is just that -- fraudulent. It doesn't reflect reality. "Low" and "high" are relative terms. Relative to what? The Austrian school knows -- market rates!

It doesn't matter all that much whether interest rates are low or high, or rising or falling. What matters is whether money is being created or destroyed to influence the interest rate away from its market value. Right now, this very instant, the FED is destroying money while pretending to be "accomodating." Bernanke is behaving perfectly in character in doing this, as it is exactly what he has done in the past. He is being as tight as he can be, attempting to extricate himself from the FED's bloated balance sheet without visibly impacting markets. He won't be able to. The assets he bought cannot be sold in any meaningful volume without triggering a financial backlash and recession.

The money supply is falling very slightly, and the rate is what it is. The FED is not supporting financial markets. If it keeps to its present course, expect them to fall. When the free market assigns an interest rate of near zero, things are really, really bad.

So long as the public believes in this illegitimate system, it will never grasp the fact that virtually all financial calculations made under the monetary pretenses of a central bank are incorrect. Just a little bit of common sense should reveal this to even a mediocre intellect. Yet the delusion persists. Why does the public believe this charade? A few days ago, I would have called it a conspiracy. But it seems that is not the proper term.

Maybe I'll address the issue, at least to the best of my abilities, some other time.

Yes, that's right, I said it -- deflation. The charts don't lie.

But note that this is a deliberate policy of the FED, not some spontaneous, out-of-control money-destroying spiral envisioned by the deflationists. It is also a small event, and might easily be reversed in coming weeks.

Note also that this does not negate the inflationist hypothesis. It is entirely consistent. The inflationary process inevitably creates inconvenient price distortions that must periodically be squelched by monetary tightening. I do not know what particular effect disturbs the FED at this time, but it appears to be taking action. If the trend continues, expect a major recessionary event, followed by a reinvigorated policy of monetary inflation.

But in the short run, bulls -- beware the matador's cape! Pay no attention to the FedFunds rate, for it only serves to conceal and distract attention from the deadly prick. It is meaningless. Bernanke is playing the same game he played in 2007. He claims to keep the rate "low" while refusing to add to the money supply. But the astute will know what this means -- Bernanke does not drive the rate lower. The market itself does. The FED is deflating, but Bernanke claims to keep the rate low and gets to play innocent bystander while the market crashes.

Or rather, to be somewhat more precise, the market distortions which have already occurred are finally revealed upon stabilization of the money supply.

The whole ruse works, of course, because the public believes in the interest rate narrative and the legitimacy of fiat currency regimes. I think even the FED believes it. It doesn't seem to occur to them that fraudulent accounting is just that -- fraudulent. It doesn't reflect reality. "Low" and "high" are relative terms. Relative to what? The Austrian school knows -- market rates!

It doesn't matter all that much whether interest rates are low or high, or rising or falling. What matters is whether money is being created or destroyed to influence the interest rate away from its market value. Right now, this very instant, the FED is destroying money while pretending to be "accomodating." Bernanke is behaving perfectly in character in doing this, as it is exactly what he has done in the past. He is being as tight as he can be, attempting to extricate himself from the FED's bloated balance sheet without visibly impacting markets. He won't be able to. The assets he bought cannot be sold in any meaningful volume without triggering a financial backlash and recession.

The money supply is falling very slightly, and the rate is what it is. The FED is not supporting financial markets. If it keeps to its present course, expect them to fall. When the free market assigns an interest rate of near zero, things are really, really bad.

So long as the public believes in this illegitimate system, it will never grasp the fact that virtually all financial calculations made under the monetary pretenses of a central bank are incorrect. Just a little bit of common sense should reveal this to even a mediocre intellect. Yet the delusion persists. Why does the public believe this charade? A few days ago, I would have called it a conspiracy. But it seems that is not the proper term.

Maybe I'll address the issue, at least to the best of my abilities, some other time.

Yes, that's right, I said it -- deflation. The charts don't lie.

But note that this is a deliberate policy of the FED, not some spontaneous, out-of-control money-destroying spiral envisioned by the deflationists. It is also a small event, and might easily be reversed in coming weeks.

Note also that this does not negate the inflationist hypothesis. It is entirely consistent. The inflationary process inevitably creates inconvenient price distortions that must periodically be squelched by monetary tightening. I do not know what particular effect disturbs the FED at this time, but it appears to be taking action. If the trend continues, expect a major recessionary event, followed by a reinvigorated policy of monetary inflation.

But in the short run, bulls -- beware the matador's cape! Pay no attention to the FedFunds rate, for it only serves to conceal and distract attention from the deadly prick. It is meaningless. Bernanke is playing the same game he played in 2007. He claims to keep the rate "low" while refusing to add to the money supply. But the astute will know what this means -- Bernanke does not drive the rate lower. The market itself does. The FED is deflating, but Bernanke claims to keep the rate low and gets to play innocent bystander while the market crashes.

Or rather, to be somewhat more precise, the market distortions which have already occurred are finally revealed upon stabilization of the money supply.

The whole ruse works, of course, because the public believes in the interest rate narrative and the legitimacy of fiat currency regimes. I think even the FED believes it. It doesn't seem to occur to them that fraudulent accounting is just that -- fraudulent. It doesn't reflect reality. "Low" and "high" are relative terms. Relative to what? The Austrian school knows -- market rates!

It doesn't matter all that much whether interest rates are low or high, or rising or falling. What matters is whether money is being created or destroyed to influence the interest rate away from its market value. Right now, this very instant, the FED is destroying money while pretending to be "accomodating." Bernanke is behaving perfectly in character in doing this, as it is exactly what he has done in the past. He is being as tight as he can be, attempting to extricate himself from the FED's bloated balance sheet without visibly impacting markets. He won't be able to. The assets he bought cannot be sold in any meaningful volume without triggering a financial backlash and recession.

The money supply is falling very slightly, and the rate is what it is. The FED is not supporting financial markets. If it keeps to its present course, expect them to fall. When the free market assigns an interest rate of near zero, things are really, really bad.

So long as the public believes in this illegitimate system, it will never grasp the fact that virtually all financial calculations made under the monetary pretenses of a central bank are incorrect. Just a little bit of common sense should reveal this to even a mediocre intellect. Yet the delusion persists. Why does the public believe this charade? A few days ago, I would have called it a conspiracy. But it seems that is not the proper term.

Maybe I'll address the issue, at least to the best of my abilities, some other time.

Sunday, January 17, 2010

Market Update

Many apologies for my prolonged absence. Life seems to have hit a rough patch. Maybe someday the lesson will sink in that life is the rough patch, and that the successful learn to take it in stride. But for now, I'm going to mope about it and let it interfere with my bloggerly duties.

At any rate, here is a quick rundown of moderately significant recent market happenings that you, intrepid reader, should know about.

The FED

Bernanke once again denied that the FED had any responsibility for inflating the housing bubble and causing the financial crisis. It wasn't the torrent of money that caused prices to rise to the moon and instigated a financial feeding frenzy. No:

“Stronger regulation and supervision aimed at problems with underwriting practices and lenders’ risk management would have been a more effective and surgical approach to constraining the housing bubble than a general increase in interest rates,”he says. It was entirely the fault of that cursed free market, you see. You can't just let people do what they please and expect the world to keep spinning on its axis, at least if your going to run a proper utopian scheme. You can't have a free market and a central bank. Raising interest rates and stabilizing the money supply just wouldn't have done the job. It would have had consequences, namely, that the country would have had to face economic reality. What you need is tighter regulations, more oversight, to make the central planner's dream work. We will achieve Utopia here, and you will do what you're told! AND SMILE DAMMIT! Note to idiot bureaucrats and politicians out there: it is difficult to defend yourself from charges of incompetence when the very thing for which you are responsible goes to the dogs on your watch. When you are running the show and things go wrong, it is, in fact, your fault. You will never, ever, be able to control it all. So, if you don't want to be blamed for every disaster that crops up, stop seeking to control every aspect of our lives! If the FED weren't in charge of running the economy, it wouldn't be blamed when the economy went into meltdown. Case closed. China Jim Chanos, short-seller extraordinaire, has chimed in that he thinks China is headed for a crash:

As most of the world bets on China to help lift the global economy out of recession, Mr. Chanos is warning that China’s hyperstimulated economy is headed for a crash, rather than the sustained boom that most economists predict. Its surging real estate sector, buoyed by a flood of speculative capital, looks like “Dubai times 1,000 — or worse,” he frets. He even suspects that Beijing is cooking its books, faking, among other things, its eye-popping growth rates of more than 8 percent.You have seen my reasons for believing China is likely headed for disaster in the short term and long term stagnation. I dealt with decidedly broader issues, but even focusing on the financial side of things as Chanos appears to be doing, things don't look good either. One simply doesn't inflate at 28%, have the government write stimulus checks equivalent to 18% of GDP, then suddenly tighten monetary policy and not get a nasty market hangover. You'd think that more folks would be in the China bear camp, but all the same, it is nice to be in the company of at least one actual investing genius. By the way, how is it that Thomas Friedman actually manages to sustain a career writing financial columns?

[I]t is easy to look at China today and see its enormous problems and things that it is not getting right. For instance, low interest rates, easy credit, an undervalued currency and hot money flowing in from abroad have led to what the Chinese government Sunday called “excessively rising house prices” in major cities, or what some might call a speculative bubble ripe for the shorting. In the last few days, though, China’s central bank has started edging up interest rates and raising the proportion of deposits that banks must set aside as reserves — precisely to head off inflation and take some air out of any asset bubbles. And that’s the point. I am reluctant to sell China short, not because I think it has no problems or corruption or bubbles, but because I think it has all those problems in spades — and some will blow up along the way (the most dangerous being pollution). But it also has a political class focused on addressing its real problems, as well as a mountain of savings with which to do so (unlike us).So, ummm..., China has a super easy money policy, and, then ... it ... ah, it goes and tightens said policy, but ...er, umm..., well Chanos just somehow isn't going to make any money shorting the market because he's just wrong. Go China! The fact that China's central bank is "edging up interest rates and raising the proportion of deposits that banks must set aside as reserves" is exactly why asset prices will fall at some point and Chanos will indeed make a lot of money if he has shorted them. It doesn't matter that a stable money supply is the correct policy and the PBoC is right to move in this direction, when you inflate prices with a credit binge and then throw on the monetary brakes, prices fall. It's not rocket science. Thomas Friedman couldn't possibly make a better case for shorting the Chinese market. Banking and the Housing Market If we are to believe certain government pronouncements, always risky thing to do, several big changes appear in the pipeline that are extremely bearish for the financial and housing markets. The FED has pledged to stop buying mortgage securities at the end of March. The housing tax credit is scheduled to expire this year as well. So far, our keepers in Washington have been holding the line on this declaration, unlike previous pledges to end the stimulus at various dates through 2009 which were all broken as it became apparent that this would put markets right back into contraction. The Austrian theory of the business cycles states that once capital prices become inflated due to an increase in the money supply, propping them up will only be possible with further increases to the money supply, so that continual increases are necessary to sustain a market boom. This is why stimulus doesn't work: the stimulus must remain permanent to have the desired effect. Keynesian's don't believe this; they think that a liberal fiscal policy can tide the market over until it finds sustainable footing. IF the FED honors its pledge, an admittedly big IF, I guess we'll get to find out who is right. I'm not holding my breath, though. Yesterday, Dear Leader Obama announced that the banking system should face restrictions on bank size and activities which sent the DOW skidding 200+ points. Today, it repeated the feat. What a joke. Virtually every financial policy of government of the past century has been to favor consolidation of banks into ever larger and fewer entities and encourage ever riskier behavior. In fact, the FDIC depends on this consolidation to curtail claims against its assets, as do other "bank rescue activities" associated with the FED. They couldn't function without it. The whole point of consolidation from an accounting perspective (which is the one that matters when you're talking about bankruptcy) is to merge healthy balance sheets with the garbage accumulated by croaking institutions to produce a mediocre, bloated, but non-bankrupt super-bank. (OK, yes ALL banks are technically bankrupt. Just so the Feds don't have to seize them. That's the point.) I don't think anything needs to be said of the effects of persistent monetary expansion and easy credit, "moral hazard," and "too big to fail" policies. Suffice it to say that gigantic banks have been explicit government policy for generations. This is central to the entire regime that governs modern finance. Don't expect anything to change. As for restrictions on trading activities MAYBE THE GOVERNMENT SHOULD CONSIDER NOT ACTING AS AN INSURER FOR STUPID BEHAVIOR AND ALLOWING THE FED TO PRINT GOBS AND GOBS OF MONEY WITH WHICH TO GAMBLE. Nah. Too easy. Bottom Line Two things are working against economic recovery. First, government efforts to "stabilize" markets are preventing prices from reaching market clearing levels. The result is a general seize-up, unemployment of capital and labor, and stagnation. Second, in an effort to keep the transactions flowing and prevent a breakdown of the banking system, the FED is expanding the money supply to provide cheap, subsidized credit and the government is running fiscal deficits to "spur aggregate demand," in Keynesian parlance. This means that transactions are taking place under deceptive conditions that do not reflect true market forces. They therefore are not generating wealth in an efficient manner and are a waste of resources. But room for monetary expansion is running out. Wages fell last last year while consumer price inflation was up around 3 percent. If you ask a Keynesian, that is not supposed to happen. If you ask an Austrian, prices should only rise when bidders, consumers in this case, have more money in their pockets with which to bid. So, where's the money coming from if wages are down? Hint -- one word, two syllables, starts with a W. Government spending is also an acceptable answer (oops! gave it away.) There's your stimulus for you -- higher prices, stagnant employment, government fostered dependency. The time is close at hand that the FED will likely curtail its expansion in response to pricing pressures. It may already be upon us. My expectation is another round of tightening, with consequent falling capital goods and commodity prices (houses, stocks, gold, etc.) and another round of layoffs. Private debt will contract as borrowers go into default. Government debt will expand as tax revenues fall and more stimulus and bailouts demand heavy borrowing. After the round of tightening and consequent recession, the FED will expand the money supply again, and we'll likely start another round of phony recovery at an even higher price than the last one. A greater fraction of the price increases due to monetary inflation will be seen in consumer prices rather than capital goods, e.g. housing and the stock market. The net result of these activities will be to slowly put ever more of the population on the dole, frustrate private wealth creation, increase the government's footprint, and erode savings, the standard of living, and the value of the dollar. When will the final inflation come? I don't really know. Maybe the next round is it. But one thing is certain -- the present is unsustainable and the government will not be able to pay its bills. Something will have to give, and every indication is that it will be the dollar. ...and, on the bright side, eventually the government.

Friday, January 1, 2010

The Next Round?

It appears that Aaron may well have been spot on in his fine post concerning predictions for 2010. I have been bearish for a number of years, but I have a very hard time spotting exactly when the corners will be turned. The stock market rally that began in March was to be expected, but its timing, magnitude, and duration caught me completely by surprise. I have learned my lesson and try to keep my predictions relatively broad. But a fair number of indicators appear to be pointing to mid-2010 as a very trying time for the economy, more akin to 2008 than 2009.

Some of these indicators I mentioned last time. The accumulation of copper inventories puts the lie to positive manufacturing data, but a substantial fall in prices will be needed to confirm this suspicion. Prices continue to rise in the face of building inventories, a strange phenomenon that should heap doubt on the nonsense about recovery and more than hint at the real source of what we see.

But possibly the biggest threat is to the financial sector, and, once again, the mortgage market. In case you haven’t yet encountered it, here is one of those semi-famous graphs that has the finance commentariat in a tizzy:

(click to enlarge)

Notice the lull in mortgage resets through 2009. A “mortgage reset” is a contractually specified time point at which the up-front “teaser rates” for an adjustable rate mortgage expire and higher rates set in, rendering payments higher. For whatever reason, fewer resets for 2009 were written into contracts, so there has been a reprieve in foreclosure activity for about a year. But we sit on the very cusp of a return to 2008-level conditions. Expect foreclosure activity to pick up again in 2010, with consequent strain on the financial system.

This time around, though, we’ll already have 10+% unemployment, Washington will have much lower tax revenues to work with, housing prices will already have taken a hit, and our financial system will already be against the ropes.

It appears that Barney Frank and the rest of our keepers on Capitol Hill are prepared. They have authorized up to $4 trillion in additional bailouts (ht. Vox Day) from the FED “just in case” there is another incident as we experienced in 2008, which tells me they fully expect another financial emergency and don’t want to be caught with their pants down this time. I guess they’d rather it was our pants.

What will be the outcome of all of this? I’m leery about predicting too much, because so much is simply arbitrary, being as it is in the hands of our democratically elected overlords to determine. I suspect we will see another round of dollar strength, as, once again, people can’t pay their bills and cash becomes king. I repeat: that is a very different proposition from actual deflation, as I have no doubt that the FED will have the money spigots wide open. But we’re talking supply and demand here, and when everyone is desperately selling off their assets to acquire the cash to pay bills, cash is what’s in demand. Which is one of the reasons politicians want to print it in the first place. I expect that this will be the case until debt levels are substantially reduced, a state which I expect will largely be achieved almost exclusively through default, both outright and through money counterfeiting, not legitimate savings and paydown of debt.

One needs cash to pay bills, but one needs property to escape inflation. Safe, secure property, not paper. As long as present money printing is marginally less than present demand for paying bills, the CPI will be relatively tame. But once we get to the stage that the primacy of security against the bill collector has yielded to security against Bernanke’s printing press, the inflation will finally be revealed to all and sundry. Only some of us will have known the real causes and that the die was cast far sooner.

But I don’t expect we’ll get there in 2010. I certainly hope we don’t. However, I could easily be wrong. I’m only an amateur.

So, my prediction: going forward, deficits will not fall as predicted. They will climb. I think Aaron's guidance for 2010 is pretty good. I'm going with a round $2+ trillion.

(click to enlarge)

Notice the lull in mortgage resets through 2009. A “mortgage reset” is a contractually specified time point at which the up-front “teaser rates” for an adjustable rate mortgage expire and higher rates set in, rendering payments higher. For whatever reason, fewer resets for 2009 were written into contracts, so there has been a reprieve in foreclosure activity for about a year. But we sit on the very cusp of a return to 2008-level conditions. Expect foreclosure activity to pick up again in 2010, with consequent strain on the financial system.

This time around, though, we’ll already have 10+% unemployment, Washington will have much lower tax revenues to work with, housing prices will already have taken a hit, and our financial system will already be against the ropes.

It appears that Barney Frank and the rest of our keepers on Capitol Hill are prepared. They have authorized up to $4 trillion in additional bailouts (ht. Vox Day) from the FED “just in case” there is another incident as we experienced in 2008, which tells me they fully expect another financial emergency and don’t want to be caught with their pants down this time. I guess they’d rather it was our pants.

What will be the outcome of all of this? I’m leery about predicting too much, because so much is simply arbitrary, being as it is in the hands of our democratically elected overlords to determine. I suspect we will see another round of dollar strength, as, once again, people can’t pay their bills and cash becomes king. I repeat: that is a very different proposition from actual deflation, as I have no doubt that the FED will have the money spigots wide open. But we’re talking supply and demand here, and when everyone is desperately selling off their assets to acquire the cash to pay bills, cash is what’s in demand. Which is one of the reasons politicians want to print it in the first place. I expect that this will be the case until debt levels are substantially reduced, a state which I expect will largely be achieved almost exclusively through default, both outright and through money counterfeiting, not legitimate savings and paydown of debt.

One needs cash to pay bills, but one needs property to escape inflation. Safe, secure property, not paper. As long as present money printing is marginally less than present demand for paying bills, the CPI will be relatively tame. But once we get to the stage that the primacy of security against the bill collector has yielded to security against Bernanke’s printing press, the inflation will finally be revealed to all and sundry. Only some of us will have known the real causes and that the die was cast far sooner.

But I don’t expect we’ll get there in 2010. I certainly hope we don’t. However, I could easily be wrong. I’m only an amateur.

So, my prediction: going forward, deficits will not fall as predicted. They will climb. I think Aaron's guidance for 2010 is pretty good. I'm going with a round $2+ trillion.

(click to enlarge)

(click to enlarge)

{kind=link}

Subscribe to:

Posts (Atom)